ESSENTIAL READING

Culture Is Captain

Why the Arsenal captaincy matters

When I was growing up in the 1970s and 1980s, Frank McLintock was already part of Arsenal folklore.

The man who led the team to the European Fairs Cup and then the Double, he was a gentleman off the pitch and a warrior on it.

Kenny Sansom was the captain as my interest grew and led by example, his excellence as a left-back never in doubt.

But it was the emergence of Tony Adams as captain in 1988, when just 21 years old, that set the stall for a generation of success.

Adams led by example, putting his head where others wouldn’t even put their feet if it meant making a clearance or bundling the ball into the opposition’s goal from a corner.

The fact that he lifted the title in three different decades says it all about his level of consistency, particularly given his own personal issues and the widespread ‘donkey’ abuse he got from fans and the media when he made a mistake.

Adams had been captain for a decade by the time the club lifted their second Double in 1998, in Arsene Wenger’s first full season in charge.

Adams embodied that warrior culture, an attitude that inspired his team-mates, but he also had a softer side, knowing who to bark at and who to put his arm around.

While he marshalled the defence, it was his guidance of Dennis Bergkamp that set the stall for that trophy haul.

Seeing Bergkamp sitting alone on the bus, he told the Dutchman: “You've been here two-and-a-half years, Dennis. Isn't it about time you won something? It would be a shame not to, with your ability.”

That may well have inspired Bergkamp, who had already grown used to Adams and other members of the back four kicking lumps out of him in training to toughen him up for the rigours of English football.

“We kept people like Bergkamp on their toes, we improved them by testing them and if they didn’t test them in training, they might not have got to the level where they’ve got so we were doing them a service,” Adams said.

Lee Dixon said recently that the rare occasions that Adams praised him on the field, calling him “One heck of a full-back” was one of his proudest moments.

Undoubtedly, Adams benefited from his defensive colleagues, Dixon, Nigel Winterburn, Steve Bould and Martin Keown, who were all cut from a similar cloth, setting uncompromising high standards that set the tone for everyone else.

Patrick Vieira was a natural successor, leading the team to more trophies and the Invincibles title, but there’s an argument that those who have followed have not been of a similar disposition.

Thierry Henry was a great in his pomp, but perhaps lacked some of the people skills to be a real leader for the varying playing personalities and we have had a succession of captains who have left the club after two or three seasons.

Adams talked about living by a set of principles that set the culture of the club.

It’s no coincidence that Mikel Arteta was captain on the day we broke our trophy drought by winning the FA Cup in 2014 and in his absence, Per Mertesacker did the same a year later.

Granit Xhaka is a Marmite player, loved by some and disliked by others, and while he may well have his limitations on the field, his appointment as captain made sense given his reputation as a leader in the squad.

But his meltdown after being booed off as he sauntered off against Crystal Palace underlined a fragility the likes of Adams and Vieira simply didn’t have.

Culture has been a key tenet of the Arteta managerial reign, so it’s no surprise that he took possibly the biggest gamble of his tenure by dropping club captain Pierre-Emerick Aubameyang ahead of the North London Derby.

Shots of our leading striker sitting, sullen-faced, and then reportedly driving off without taking part in the warm-down after the game, may have been the result of Arteta’s slightly naïve admission that Aubameyang had been dropped.

Whether reports of lateness are true, the Arsenal captain has to set the example which others follow and it comes back to the culture that develops from the top of the club’s playing staff all the way down to the youth teams.

Aubameyang is undoubtedly Arsenal’s biggest star but then again the same could be said of Thierry Henry or Bergkamp when Adams wore the armband.

During the 2-1 victory over Tottenham, Kieran Tierney set the standards by tearing Matt Doherty apart down the left in tandem with Emile Smith Rowe.

It was fascinating watching the player-cam footage Arsenal shared after the game of Tierney barking orders at his team-mates, bombing forward or making tackles for the Arsenal cause.

Much has been made of Tierney’s ‘Braveheart’ attitude, the down-to-earth shopping bag persona made true by his refusal to wear warm training gear in Arctic conditions when shorts and a t-shirt would suffice.

But it’s not just his choice of attire that sets Tierney apart.

He’s clearly cut from the same cloth as McLintock or Adams, a player proud of his colours who expects others to follow the standards he sets.

Just as Adams had done with Bergkamp, Tierney is reported to have unsettled some team-mates with his aggressive and full-throttle approach to training when he first arrived.

But isn’t that precisely the level of commitment, determination and passion that we want to see from our captain?

Don’t we want our captain and indeed every player to exert the same effort that we fans would if we were suitably fit and skilled to do so?

At the very most, Aubameyang has two years left as Arsenal captain and Tierney’s credentials as his successor are indisputable.

When Arteta talks about the culture of the club and non-negotiables, Tierney ticks every single box.

Arsenal Need To Look Forward To Compete Again

In the dark days towards the end of George Graham’s reign at Arsenal, when the flair and excitement of his earlier teams had given way to fearful pragmatism, our football was essentially route one, hoping for Ian Wright to do something special.

Graham eventually signed Chris Kiwomya and John Hartson, neither of whom lasted very long, and it was not until the arrival of Dennis Bergkamp and Arsene Wenger that we became a dynamic attacking unit once again.

Bergkamp was undoubtedly a generational talent, providing the ammunition for Wright, who only dropped below at least a goal every two games in his last season with the Gunners.

I saw an interview with Wrighty recently where he spoke of his regret that Christopher Wreh came on in the 1998 FA Cup final rather than him for what would have been his final appearance in an Arsenal shirt at the age of 34.

But while Wenger could often be criticised for his defensive acumen, he collected forwards like candy – and he made a decision in that title-winning season that Wright was declining.

First it was Nicolas Anelka, then of course Thierry Henry who caught the headlines as leading goalscorers.

But Wenger supplemented them with the likes of Kanu, Sylvain Wiltord, Francis Jeffers, Robin van Persie and Emmanuel Adebayor.

With the exception of Jeffers, who didn’t make it, and van Persie who rejected a new contract, Wenger knew when to sell or release his forwards to ensure he had a fast and energetic front line.

Whether we played with a number ten such as Bergkamp or relied upon the pace and drive of our wide players, the forwards adapted and thrived whenever called upon.

Questions have been asked this season of the wisdom of giving Pierre-Emerick Aubameyang a new contract and whether it’s a reward for what he has done rather than what he will do.

Given his struggles in front of goal this season, those concerns have some justification, even though the team’s greater attacking challenges have undoubtedly had a role to play.

But you only have to look at how reluctant he is to press and his dip in efficiency to see that he needs to become strategic in his exertions.

It was only a few weeks ago that Alexandre Lacazette was being written off before his recent renaissance pulled us out of the mire – but his limitations in Arteta’s system are clear for all to see.

The Premier League has been so tight this season that finishing in the top six is not impossible, however fanciful a prospect that may seem as Arsenals’ form lurches from sublime to ridiculous.

The Europa League looks particularly strong this season but still offers a route to the Champions League that the club so desperately want and need.

The problems the club have faced in recent years are well documented: signing players who then no longer deliver on long, costly deals; and letting contracts run down, giving us little choice but to sell or exchange or release talents for way below their market values.

That’s why this summer is so important for Arsenal and why Edu and his trimmed-down team of scouts and analysts need to be putting plans in place now.

We have exciting, forward-thinking midfield talents such as Bukayo Saka and Emile Smith-Rowe – and granted, more creativity is desperately needed – but we need to supplement them with younger strikers who have the intensity and desire to take us to the next level and beyond.

Arsenal need to be brave – and that means making wholesale forward departures at the end of the season.

Aubameyang will still have two years to go on his contract, so we can extract some value from him if we decide to sell him even if he will be 32 at the end of June.

Lacazette will be 30 in the summer with only a year left on his current deal and will want big money to extend.

Then we have Eddie Nketiah who has not yet done enough to convince that he can be a prolific striker at the very highest level, despite his superb record for the England under-21s. If West Ham, Brighton or any other top-flight club offers us north of £20m for him, he should go.

Nicolas Pepe has appeared to be weighed down by the size of his transfer fee, but, just as with Willian, who has no such fee to burden or blame for his performances, he has often appeared to be a poor fit for the club.

His recent improvement no the left suggests green shoots are finally emerging, but as with Lacazette, can he really contribute consistently in Arteta’s system and in the Premier League?

Such a dramatic front-line overhaul, coming alongside necessary midfield recruitment, may appear drastic.

But we could reasonably expect close to £100m in sales for those mentioned, presuming we got around half our money back on Pepe if Arteta decides to cash in.

There’s money to be made from Mattei Guendouzi and Lucas Torreira as well, don’t forget.

I still hold out hope that we can convince Folarin Balogun to stay, his fleeting appearances suggesting that he could be a special talent with a keen eye for goal.

Few would argue that Gabriel Martinelli looks to be a world class player in the making – if we can keep him fit – and a player who can become a key striker for us.

With Celtic waning, perhaps Odsonne Edouard might want to test himself in the Premier League while former Gunner Donyell Malen continues to impress in Holland.

The Premier League is characterised by speed and energy, so a forward line of 30-somethings is always going to have its weaknesses.

Just as in midfield, Arsenal need athletes with intelligence, drive and the hunger to win that may be fading as our older players enter the twilights of their playing careers.

Hopefully Edu is already putting plans in place so that this time next season, we are truly competitive once more and establishing a core of younger players who can help us challenge for the title and Champions League progression rather than short-term solutions whose limitations have been clear for all to see.

Progress in January Means Reevaluating Edu's Performance

The last few years have undoubtedly been times of great upheaval at Arsenal. You can go back to the Champions League final in 2006 as the peak of Arsenal as a top club. We may have flirted once or twice since with title tilts, but we were burdened with a hugely expensive new stadium.

Was it the stadium, though or the departure in 2007 of David Dein, the club’s power broker, transfer fixer and Arsenal visionary? It left Arsene Wenger without his trusted Lieutenant, a man who could push through new signings or pull back from potential mistakes. He wasn’t perfect, of course, but then the nature of football means transfer perfection is nigh-on impossible. For every Sol Campbell or Nicolas Anelka, world class players bought for very little, there were mis-steps such as going low on Ashley Cole’s contract renewal which saw him ultimately leave the club for Chelsea; or sign Francis Jeffers for a big fee.

Wenger’s reign had undoubtedly gone stale by the time of his departure in 2018, with plans to spread the workload and responsibilities stuttering to say the least. Perhaps it was to be expected when the club had operated in one way for a decade with power unhealthily concentrated on the shoulders of one man.

In the next 18 months or so after Wenger’s departure, we lost Ivan Gazidis (despite justifiable questions about his own abilities), Sven Mislintat and Raúl Sanllehí, with Vinai Venkatesham taking the role of CEO. To say it has been a time of upheaval is an understatement, and one which many fans expected, but perhaps not quite as tumultuous as it turned out to be.

When he was appointed late in 2019, Mikel Arteta was tremendously impressive, talking about Arsenal as a big club, the “non-negotiables” and the winning mentality that we so desperately needed. To expect a rookie coach to get everything right in his first year is perhaps too much to ask – even though the FA Cup victory, joyous as it was, masked some of the inconsistencies and mistakes that became more apparent during our terrible run before Christmas. Arteta has remained steely-eyed throughout his first year and few would argue that his first year has been a challenge.

Punctuated by lockdowns and financial challenges caused by the Covid-19 pandemic, no wonder Life President Ken Friar, who has been associated with the club for more than 70 years, described 2020 as the most difficult year in the Gunners' history. We now live in an era of impatience, where big clubs hire and fire coaches as soon as things start to go wrong – hire fast, fire faster. But sometimes the ‘project’ needs time to mature before pulling the trigger.

Which brings me to Edu and his importance to the club.

A decent midfielder for Arsenal, he was brought in as the club’s technical director and has now essentially become the Dein to Arteta’s Wenger. He was tainted when he first arrived by his association with Sanllehí and an unhealthy connection to certain agents. Having proclaimed that all transfer business had to go through him when Sanllehí departed, the Brazilian has been tarred with some of the contractual impasses that have seen the club lose millions in potential transfer fees.

A year after we signed David Luiz, whose error-strewn spell at Arsenal has often been disappointing, much was made of the signing of Willian, another Chelsea veteran expected to help us push for the top four as quickly as possible. Willian has been an unmitigated disaster and we are lumbered with a three-year contract for a player so far from his peak that his summer 2021 departure must be a priority.

Dein would most likely have stopped the Willian signing, urging focus on nurturing Reiss Nelson or looking at a younger option, should transfer finances have allowed. Edu has to take some responsibility for those errors. The Arsenal strategy has to be on buying long-term players with a high ceiling rather than washed-up veterans who appear set for comfortable retirement paydays.

But with the closure of the winter transfer window, it’s time to take a step back and accept that, on balance, Edu has already been a success. There are so many signings he has made in the first 18 months who have already proved their worth.

Perhaps Edu did not make enough about his reported involvement in the £6m deal to bring Gabriel Martinelli to Arsenal. In the Brazilian forward, we have a young, exciting forward who made an instant impact and who has the potential to be a genuinely world class striker. If he reaches the heights he looks capable of, Martinelli could have a transformative influence on the team and still have value to be sold for a big fee in years to come.

This time last year, we signed Cedric Soares and Pablo Mari to bolster a defence which was already packed with players. Mari has been blighted by injuries but has looked solid whenever he has played and I suspect he would have continued to play had it not been for his recent injury setback. While the evidence is limited, he already looks more accomplished than Luiz, Shkodran Mustafi and Sokratis, a trio who will all have left the club by the end of this summer.

Cedric Soares, an older full-back, has also had limited opportunities and has been labelled a mid-table journeyman. But he was brought in as an understudy for Hector Bellerin, who alongside Ainsley Maitland-Niles, was a possible departure last summer. With both of them staying as the market stagnated, was it really the worst decision to have signed an inexpensive replacement? While Cedric isn’t a long-term option, he has improved with game time this season and his display against Southampton last week proved his worth.

Of our other summer signings, are there any doubts about Gabriel Magalhães or Thomas Partey? Gabriel already looks solid and capable of improvement and despite spending much of the first half of this season on the treatment table, Partey already looks to be one of the best midfielders in the league.

Many fans have looked at Emiliano Buendía, Yves Bissouma or even Houssem Aouar to give us more strength in midfield, but the loan signing of Martin Odegaard makes absolute sense. The Norwegian playmaker already has years of top-flight experience in Holland and Spain and while his ability to manage tendonitis and the pace and power of the Premier League remains to be seen, his reputation remains as one of the most exciting young creative talents in world football. And he has signed at little cost or risk to the club but capable of sharing the creative burden with Emile Smith-Rowe.

Edu has also managed to ensure Mesut Ozil is off the Arsenal books. Whatever your thoughts on the German playmaker, his continued presence became an inconvenient sideshow and his departure allows everyone to move on.

Sokratis has also gone, as has Shkodran Mustafi, thankfully, and while it remains to be seen how successful the loans for Joe Willock and Maitland-Niles turn out to be, their departures make sense given their limited game time.

If young players are not going to make the grade or do not yet appear ready to play regularly for us, a loan will either build them up for next season or hopefully raise their value and profiles for future sales. Perhaps Nelson could have moved on loan and Lucas Torreira had his Atletico Madrid nightmare curtailed, but there’s no debate that Arsenal got a lot of work done to re-shape the squad.

If there is one black mark against Edu recently, it’s the failure to pin Folarin Balogun down to a new contract. The young striker already looks capable of making the step up and yet it looks likely that he will leave when his contract ends in the summer. But as I said at the beginning, football is not an exact science, and while it may look easy to buy and sell players, the reality is far more complex.

Arteta has already hinted that next summer’s transfer targets are already established, so it will be fascinating to see the profile of the players we bring into the club. Edu will no doubt have to prove himself all over again, but if we continue to shift the deadwood and bring in young players capable of becoming elite, the Brazilian’s stock as a transfer fixer will continue to rise.

The Kids Are Alright

by Oscar Wood (@reunewal)

During the many struggles Arsenal have faced over the course of the last two seasons, one of the few consistent positives has been the emergence of an increasingly large selection of talented young players. While the hype around any young footballers who show signs of promise is rarely lacking at the best of times, the situation at Arsenal has only led to this being intensified. Starting from the Europa League group stage last season, the performances of these younger players has often been in contrast to the struggles of older, more highly paid players, who have themselves been underperforming. What more, with Arsenal currently looking as far away from the elite of European football as they have been for decades, the idea of talented academy products and youth signings provides an element of long term hope that simply doesn’t exist in the short term.

Arguably the most impressive performer so far, as well as the most exciting prospect is Bukayo Saka. Not only has he been a consistent starter and one of the best performers for Arsenal in the Premier League for a year now, he’s also a talent with few clear limitations and boundaries when it comes to his development possibilities. Left back, left wing, right wing, weird left wing-back/left sided interior hybrid, Saka has flourished to various extents playing all of them. What more, his mastery of these different roles is only growing. Just two weeks ago I tweeted scepticism that the right wing would be his ultimate position, only for him to put in probably his most complete right sided performance of his senior career in the next game at West Brom.

In some ways, it’s this versatility of Saka that entices people the most. One of the reasons fans love young players in the first place is that there are fewer constraints to what they could become. Even top quality older players are restricted to their strengths and weaknesses that are unlikely to change much. With a youngster of Saka’s ilk this isn’t the case, fans can envisage almost any future they want for the player.

The number of best case scenarios that have been suggested for his future peak are countless: a cut-in and shoot scorer and creator from the right (Arjen Robben), a dynamic outside winger on the left (Leroy Sane), a creative interior (David Silva), a versatile box-to-box player (Blaise Matuidi), a dynamic left-back (Alphonso Davies), a Swiss army knife left sided player (Raphaël Guerreiro).

Of course, Saka still has to make significant progress in his development if he’s to reach the heights any of those players have, but the signs are good at such a young age. He has shown some good off ball movement, an ability to create his own shots and an eye for a final ball that suggests he could become a prolific forward. His xG + xA per 90 in the league this season is 0.4, bettered only by Ferran Torres and Phil Foden for players under 22 in the Premier League.

In terms of his general play, he has been an integral part in the build of multiple goals - both v West Ham, and the equaliser v Southampton - with his dribbling and passing. If he is to become more of an outright midfielder the next step is arguably to simply get on the ball more, as he’s shown he has the quality to do good things with it. Arsenal have lacked a high touch attacking player post-Özil and Alexis, someone you can give the ball to against a set defence in hope of inspiration. That has often been Saka this season but it has usually come in flashes rather than across 90 minutes. It could, however, simply be a case that the team improving and becoming more dominant will see Saka become that player.

Rather than pigeonholing him into one role and assessing his development relative to that, it seems best to simply let him grow, and only fix a role for him based on the aspects of his game that continue to improve.

Gabriel Martinelli’s game is a lot more simple. Since his move to North London, he has proven to be very effective at getting on the end of moves for a teenager in his first season playing at the elite level, and has been an incredibly committed and hard working presser. It is the latter that has helped endear him so much to fans. His energy and determination is infectious and is the sort of thing that can lift his teammates as well as fans.

He is, however, still incredibly raw, which isn’t a surprise or a criticism given it’s only 18 months ago that he came to the club from the Brazilian fourth tier. There have been obvious comparisons between him and Alexis Sanchez, Arsenal’s last superstar South American forward. The comparison fits in the position they play and the attitude and personality they play with. Martinelli, however, hasn’t shown much to suggest he can be the ball dominant, dribbling, creative force that Alexis was at Arsenal. There’s room for that side of his game to grow, however, and even without it, he’s still good enough to be a useful Premier League player at 19 thanks to his athletic capabilities and his movement.

It’s at this point worth noting that expecting Martinelli to reach the next level in the next season or two probably isn’t realistic. There are many examples of current Premier League attackers - Raheem Sterling, Marcus Rashford, Christian Pulisic - who broke through as capable starters at the age of 18 and mostly stayed at that level for a few years before reaching another level in their early 20s. For Gabi the next couple of years will be about building minutes, and Arsenal fans will likely have to put up with his current deficiencies once his new prospect shine begins wearing off - which history suggests will happen.

Peter (@ThatGooner) has done a comprehensive analysis on Martinelli that looks into the micro details of his game that is worth reading.

Emile Smith-Rowe is probably the player with the most immediate upside for the team, since the squad has no other player who provides the same skills or operates in the same zones of the pitch.

Smith-Rowe looks very much like the archetype modern number 10. Like Saka, he has demonstrated an impressive level of footballing intelligence when it comes to his movement and choice of pass, but he also has the level of athleticism needed to be a threat in transition, both in carrying the ball at this feet and in the runs he can make off it. The Saka goal at West Brom was probably the most encouraging bit of play in Arsenal’s season, and the best example of Smith-Rowe’s most important qualities. He plays a first time line breaking pass and then immediately sprints into the space in behind. It’s the kind of pass and move play that has been so lacking in recent times.

While it’s the potential creative upside of his game that excites people the most, I wouldn’t be surprised if it’s his carrying of the ball and his goal scoring threat that becomes his best asset. From the limited amounts of him I’ve seen at Arsenal and in highlights for Huddersfield, his passing seems competent for a Premier League number 10 rather than potentially special. That said it really is too early to make definitive judgements. He has still played only five Premier League matches in his career. Now that he has established himself very much in the first XI picture, he needs to finally have an extended run of staying fit before we can make more clear judgements.

The flip-side of the rise of three three over the last year has been the scaling back of expectations for the 99 generation of Hale End products, all of whom are 21 and are yet to establish themselves as should be starters. That, however, doesn’t mean they no longer serve value.

Eddie Nketiah could fairly make a case that he is the rarest of things, an under-hyped academy product. While he lacks the traits of a future superstar, at 21 he has already proven himself to be competent at the hardest skill in football; scoring goals. Both last season and this season his non-penalty xG in the Premier League has been fractionally better than Aubameyang’s. While Arsenal’s Europa League group this season was particularly weak, Nketiah still dominated it, scoring 3 and producing over 4 xG from 20 shots within the box. No other Arsenal player who played the group stage was able to get close to as many good shots off. Even his failure to get starts ahead of Patrick Bamford at Leeds last season looks a lot less damning now than it did then.

Nketiah probably won’t become a striker good enough to lead Arsenal where they want to be, but he is likely already close to being a bottom half Premier League starter, with plenty of years ahead of him to continue to grow. For Arsenal that leaves him as a good squad player or a potential sale for a sizeable profit, like Alex Iwobi before him, who can make space for the next product on the conveyor belt, such as Folarin Balogun, to take his place in the squad.

Reiss Nelson was at one stage considered the biggest prospect at Arsenal - having won player of the season in the PL 2 as Arsenal u23 won the division in 2017/18 - but a failure to push on in the first team and the emergence of aforementioned others has seen him become something of a forgotten man. I still think he can offer value as a technically secure wide player, but it’s looking unlikely that he will become a truly prolific wide forward in the Premier League.

Joe Willock hype arguably peaked 18 months ago, and his reputation among Arsenal fans now feels very low compared to his new peers. He has reached an interesting stage of his career where he has been able to dominate the Europa League group stages, but in the PL minutes he has been given he hasn’t been able to make much impression. Now 21 it feels like he’s moved beyond loan age, but one could still be useful to a club near the top end of Championship or the lower end of the Bundesliga. Somewhere where he could play lots of minutes and the club can make a more definitive judgement on his level. It seems unlikely his passing and overall technical level will ever be good enough to be a starting midfielder for a club with top four aspirations, but he does still offer a unique profile in the squad with his off ball running from deep areas.

Moving away from the 21 and under club, the trio of 23 year olds in Kieran Tierney, Gabriel and Ainsley Maitland-Niles will also have big roles to play in Arsenal’s continue rebuild. Tierney has already become a cult hero amongst the fanbase and the last few weeks have seen his best performance level at the club. While Gabriel fell back to earth somewhat in his last few performances of 2020, his season so far remains the most promising displays from a young(ish) centre back at Arsenal since probably Laurent Koscielny’s debut season. The hope is that those two will form the left side of Arsenal’s defence for years to come. Maitland-Niles remains in an interesting place. In only a year Arteta has flip-flopped on his use of Maitland-Niles multiple times. While it’s still possible he could make the right back spot his own, it seems more likely that if he’s not sold he’ll remain a valuable squad member; a versatile player who can play either fullback spot thanks to his great one v one defending.

Of course it would be remiss to mention that it’s not all been rosey with Arsenal’s younger players recently. Two years ago Mattéo Guendouzi was comfortably the most polished youngster at the club, and was already proving a fine Premier League midfielder at 19. Without getting into the rights and wrongs of his demise under Arteta, it feels unlikely Arsenal’s best young midfielder has much of a future at the club, which is a massive shame. Meanwhile William Saliba, signed for an eye watering £27 million in 2018, has essentially had six wasted months playing under 23 football. At 19 it was probably unrealistic to expect him to be ready to start in the Premier League, and the whole ordeal doesn’t mean he now can’t be a long term success at Arsenal, but the club were indecisive during the summer as to whether he was ready, and this has cost him development time.

A talented collection of young players is by no means new for Arsenal. With the likes of Cesc Fabregas, Nicolas Anelka, Jack Wilshere, Aaron Ramsey, Theo Walcott and Alex Oxlade-Chamberlain in the last couple of decades, Arsenal have had some of the best teenage players in the world at their club, guys who were key players on teams that were among the European elite. Even in more recent history, the likes of Serge Gnabry, Jeff Reine-Adélaïde, Ismaël Bennacer and Donyell Malen have been around only to fall by the wayside. This current generation is benefitting from the fact Arsenal have to lean into them, and are thus getting more opportunities to showcase their talent.

Academy products - and cheap young signings, which essentially fall into the same bracket - can serve three functions. They can provide a cheap route to a star player who would be too expensive to obtain through the market, such as Harry Kane at Tottenham. They can provide a cheap way to fill out the squad, as Manchester United did so successfully under Ferguson, something Tim Stillman has pointed out numerous times on the pod and in articles. Or they can be sold for profit, as Alex Iwobi was when he left for Everton.

In Saka and Martinelli, Arsenal have prospects that have shown signs they could become future star players. If just one of them, or someone else, can reach that level, then this crop of players will have succeeded. Most of the current 21 and under club will likely never become more than reliable starters or squad options, and that is fine. For a while now some of us have been frustrated that the club hasn’t focused more of their transfer strategy on younger players. The current success of these players show that a 20 year old prospect can be just as good, if not better, at football than an experienced player on big wages. Maybe this will be an epiphany for Arsenal’s long term rebuild.

Why Arteta should return to the 4231

by Peter Taylor (@pjtreelaw)

The 4231 has, over recent years, become viewed as a somewhat regressive formation, a formation tied intrinsically to the early 2010s when almost every team in world football operated in some variation of the shape. Arsenal fans in particular have more than had their fill of the 4231, with mid to late Arsene Wenger sides almost exclusively lining up in this formation (until his late switch to 343) and regularly shipping goals despite some fluid attacking moves. Dismissing the shape as archaic when compared to, for instance, a 433 where the midfield triangle is flipped seems wrong-headed and overlooks some of the highly innovative sides using the shape to great effect in the modern game.

The Modern 4231

When one considers the 4231 in a modern context 2 significant teams come to mind; Bayern Munich and Ajax. The two European giants use similar interpretations of the shape and both have achieved huge success relative to their budgets and expectations. Bayern under Hansi Flick operate with attacking fullbacks including the sensational Alphonso Davies usually married with the slightly more reserved Benjamin Pavard, though recently they have begun to use the slightly more adventurous Bouna Sarr whilst Lucas Hernandez replaces the injured Davies. The centre backs are typically excellent passers and relatively quick and the midfield pivot usually sees Joshua Kimmich paired with Leon Goretzka. In last season’s Champions League winning side Goretzka was often replaced by Thiago Alcantara when available. This midfield pivot can function differently depending on game state and opposition strength, with one of the pair dropping into the backline to offer additional build up options and cover against the counter if required, usually Kimmich, or with both operating on the same plane if numbers are required higher up during build up. Bayern have a plethora of attacking options, with any of Kinglsley Coman, Serge Gnabry, Leroy Sane and Douglas Costa able to play the wide positions and Thomas Müller able to play across the front line. Ahead of them Robert Lewandowski continues his astonishing goal scoring run and is ably supported by exciting youngsters like Joshua Zirkzee. In attack Bayern’s wide attackers pull into the half spaces, with fullbacks overlapping to occupy the high wide zones and Lewandowski in the centre. Behind this line of 5 Müller flits in and out, finding space to create chances for others or find opportunities for himself along with moving to create overloads, a key principal for Bayern in attack. Kimmich and Goretzka can either push up and support or remain deeper to cover and provide recycling options. The entire system is made possible by Bayern’s incredibly high line and energetic press, preventing opposition counters before they can even begin. The narrow nature of Bayern’s attacking 4 and the prevalence of overloads enable incredibly efficient pressing, with a ball turnover usually meaning the opposition player is immediately outnumbered and harried by several Bayern players in close proximity.

Ajax use a similarly aggressive high press and attacking line, again using the wide attackers in the half space when high up the pitch. Ajax also make use of overloads, with the 10 coming across to help outnumber the opposition, but often make use of quick switches to the wide player on the opposite side who, rather than being drawn inside, remains high and wide to create space on the opposite flank to the overload. In build-up they tend to make more use of a midfielder dropping into the backline to create a three, with this most apparent during the 2017-18 season when Frenkie de Jong announced himself as a budding superstar with his performances in this deep midfield role. Ajax often commit 7 players to the attack, with midfielders bursting forward to add greater fluidity and intent to Ajax’s attack. This can leave them open at times but again a high line and aggressive press can compensate for their occasional openness at the back.

Recently, the Premier League’s two finest sides have both started employing variations of the 4231, with both Manchester City and Liverpool employing the shape in their recent 1-1 draw. City have been toying with the shape for some time, allowing Kevin De Bruyne the freedom to roam more in attack than he is able to in their previous 433 and compensating the loss of peak Fernandinho in the anchor role by playing Rodri and Gündoğan in tandem. This double pivot also means that opposition teams have a harder time isolating the City pivot, meaning build-up play from the back can be more varied and harder to stop. Liverpool have often seemed to be toying with the idea of shifting to the shape, pursuing players who would seem better suited to a 4231 than their 433. The incredible form of Diogo Jota seems to have forced Klopp’s hand, with the German reverting to the shape he preferred in his Bundesliga days and has employed at times whilst at Anfield. Elsewhere in the Premier League Leicester, Tottenham, Aston Villa and to a lesser extent Manchester United have all seen recent success using the shape. Is there a particular reason the system seems to be rejuvenated in the modern game.

Changing roles rather than changing shape

Perhaps the major reason for the 4231’s fall from grace was the roles of the players used in the system. The major point of failure being the number 10. Teams in the mid 2010’s who used the shape against high pressing 433s found that employing a dedicated playmaker with little defensive contribution meant their midfields were overrun by the three in opposition. The two 8s in the 433 could harry and harass the deep pivot and 10 of the 4231, with the 10 often marked out of the game by the deepest midfielder of the 433. This decline of the archetypical number 10 is familiar to Arsenal fans, with a certain German playmaker perhaps the clearest example of a player for whom the game has simply evolved past. However, rumours of the 10’s demise have been greatly exaggerated. The best player in the Premier League over the past few years has been City’s de facto number 10, Kevin De Bruyne. Bayern’s Müller contributed over 30 goals to Bayern last season. Kai Havertz was sold for an enormous sum to Chelsea, with few questions over whether the deal was sensible due to the player’s enormous quality. What these players have in common is their tactical flexibility, incredible goal threat and creativity married to exceptional work rates and the ability to contribute to the press. The modern 4231 can allow for an attacking midfield presence simply because the players employed in these roles are no longer defensive passengers but key contributors to an aggressive press.

Arsenal in a 4231

So, how could Arsenal employ the shape to maximum effect? Frankly most of the roles seem fairly easy to fill, with many players ideally suited to the system.

Attack

Nicolas Pépé honed his talent in the wide right of a 4231 where he was allowed to drift into the half spaces. Bukayo Saka seems to have the talent to play anywhere behind the striker, with his work rate and excellent movement ideal for the system. Joe Willock’s excellent off ball movement and improving technical skill under pressure perhaps harkens to the skills Thomas Müller employs as Bayern’s Raumdeuter.

Midfield

In Thomas Partey, Dani Ceballos, Mohammad Elneny and Granit Xhaka, Arsenal have a variety of deep midfielders who could be paired based on opposition strengths and weaknesses, with a fair degree of tactical flexibility offered by the different combinations. The use of a double pivot also seems best suited to Arsenal’s contingent of deep midfielders. Whilst either Partey or Xhaka could be used as a lone pivot, the security of a deep midfield partner should bring out the best in both players. Partey has almost exclusively played in a pair at Atletico and many of his key strengths are maximised when used this way. He has greater ability to press and harry without worrying about space in behind, has more freedom to burst forward and carry the ball through the opposition midfield line and can even be afforded the chance to get in and around the box more when covered by a partner. Xhaka’s strengths in passing, build up positioning and his somewhat under rated defensive contribution can all be useful when in tandem with another, slightly more positive and press breaking partner and his weaknesses in mobility and press resistance can be lessened by a physical, press resistant partner to take the pressure of the Swiss. Ceballos is perhaps only player better suited to playing as an 8 in a 433 but has shown he is more than capable of playing as the more progressive of a midfield pair. Elneny, interestingly, actually profiles fairly well as a possible lone 6 on paper, with his discipline and simple but efficient passing game seemingly ideal for the anchor-man role. He has, to my knowledge, never played this role for Arsenal and his tireless energy for the press can also be better utilised in a midfield partnership when afforded cover by another player. Building play from the back with two pivots also prevents one being isolated and thus the build-up stymied, something City have demonstrated in their switch to the system.

Defence

Kieran Tierney and Hector Bellerin are both strong in attack and seem ideally suited to overlapping wide. The defence perhaps lacks a little pace, but Gabriel is fast becoming regarded as one of the best defenders in the league and in combination with David Luiz offers good ball progression from the back. The player who would, perhaps, gain most from this shift is Arsenal’s talisman, Pierre Emerick Aubameyang.

Attacking strengths and Aubameyang

One of the key issues with Arsenal this season has been the poor form of and poor service to Aubameyang. There has been a great deal of clamour for Arteta to shift Aubameyang to the central role in his current system but this overlooks one of the main features of the centre forward role in this shape. The striker has been predominantly dropping deeper in build-up, allowing Aubameyang to run in behind from his inside left role. This clearly has not been working of late, but simply moving Aubameyang to the centre would either mean Arsenal lose their key man closer to goal or lose a key component of the build-up. In a 4231, however, Aubameyang can remain high, perhaps even drifting a little left in search of space, whilst the 10 occupies this key position in build-up with assistance from the left and right attacking midfielders when required (Figure 1). Arsenal can then either form a front 5 with a 3-2 defensive and midfield split (Figure 2) or a 2-3 (Figure 3), shifting whether one of the pivots drops into the back line depending on opposition. This system ends up being fairly similar to Arteta’s current system when high, though the use of a more attacking midfield option means the front line can effectively become a 6 rather than a 5, and the ability for this attacking midfielder to drift and provide an extra body to create overloads or to make third man runs to find dangerous spaces should go a long way to improving Arsenal’s creativity and goal threat, the single biggest concern for Arteta at present.

Figure 1 Flexible positioning during build up in the 4231

Figure 2 The defensive 3-2 split in attack

Figure 3 The defensive 2-3 in attack

Defensive flexibility and pressing

One of the great strengths of the 4231 is that it can offer multiple options for the defensive aspect of the game. The system is ideally suited to high pressing, as previously outlined, due to the high density of players in attack. If the opposition manages to retain the ball or is starting from a goal kick, for instance, the system can retain a high press by shifting into a 442-like shape, the attacking midfielder joining the striker to press the opposition back line with the wide attackers cutting out passes to the opposition full backs and one central midfielder pushing into to press the opposition whilst the other covers his partner (Figure 4). This pressing shape has become the gold standard thanks to the Ralf Rangnick and his various disciples who have pushed German gegenpressing into the forefront or modern tactical thinking. The shape offers excellent coverage across the entire pitch and a narrow 442/4222 can control the centre of the pitch, pushing the opposition wide into pressing traps and throttling any chance of effective opposition build up. Arsène Wenger even describes the 442 as the “mathematically ideal formation” due to the fact it maximises the space covered by the team. The 442 is also famous for its deep defensive solidity, being the shape of choice for defensive, compact and aggressive sides when in a deep block, perhaps best illustrated by the Atletico Madrid sides of Diego Simeone (Figure 5). The system could even be shifted slightly, when under extreme duress, to use Arteta’s ideal coverage of the 5 attacking lanes with Bukayo Saka dropping deeper and Tierney rotating inside, Willock dropping deeper and Aubameyang and Pépé remaining counter attacking threats when facing much stronger opposition (Figure 6). This option should be used sparingly and only when under exensive pressure, but Arteta has done an excellent job of training his side to employ this sort of flexibility and it should be utilised in the right circumstances.

Figure 4 High pressing in the 442

Figure 5 The mid/low block in the 442

Figure 6 Shifting to a 5-man backine in the low block

Conclusion

Arteta has already used the system to some effect, particularly early in his reign, but has not made the tweaks I outline here yet. I believe the key shifts would be the use of a number 10 to help aid build up and free a central Aubameyang to find space in behind. A more concerted effort to press high in a 442 and more freedom for the 10 to search for space and create overloads should significantly improve the lack of creativity currently on offer. Perhaps one of the biggest shifts would be more one of mentality than positioning, with the team more committed to the back 4 than the comfort blanket of the back 5. The system can make use of the excellent developments in defensive organisation Arteta has engendered whilst taking our attacking game up a level. The system can even be tweaked in game to allow for more defensive solidity in a pinch. Clearly the addition of a top-quality attacking midfielder would further improve the system, though Arsenal has already indicated they are looking at this position with their pursuit of Houssem Aouar and links to Dominik Szoboszlai. Additions in defence or perhaps the emergence of Saliba could add further speed to help cover for the necessary defensive high line to maximise the system. However, even with the current squad the system offers significant upside and the possibility to develop our attacking game whilst retaining much of the good defensive organisation we have seen of late.

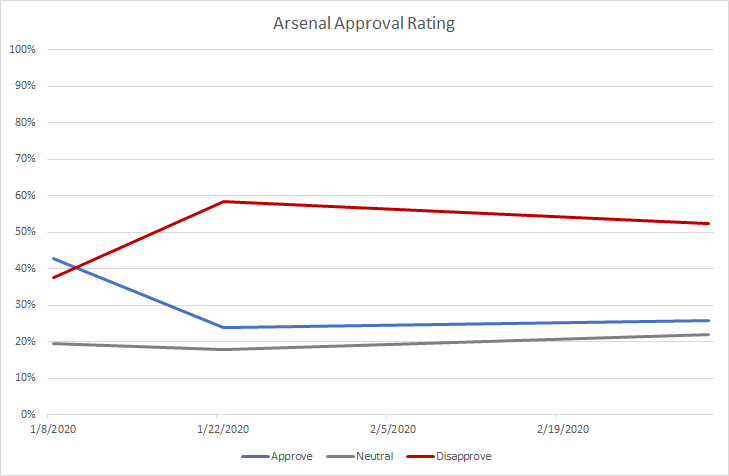

Happiness Index Report: March 8, 2020

by Scott Willis

Time for another round up of how Arsenal fans feel about the state of the club. Since I last asked about things Arsenal have played 7 matches, winning 5 of those and collecting a pretty impressive 2.3 points per match in the league (87 point pace!), won two FA cup matches while advancing to the quarterfinals but they also got dumped out of the Europa League when they really should have gone through.

GENERAL ARSENAL APPROVAL RATING:

Even with being knocked out of Europe, fans are happy with how the club is doing right now. I asked a new question this week about how people feel about the direction of the club and things are similar in that people are positive about the direction of the club.

How things have changed overall over the 3 surveys.

ARTETA APPROVAL RATING:

There aren't any complaints about Mikel Arteta.

THE MANAGEMENT DUO:

Raul still is still the second least popular figure among Arsenal management (only behind the owners) but fans' opinions didn't really get worse from him compared to the last survey.

Edu is starting to see his numbers trend more positive with people starting to move off of neutral stance as he has been at the club longer.

Interestingly people are generally happy with the overall talent level of the club but they have questions about the people who are leading the recruitment efforts.

Where people are not happy is with the ownership of Kronkie Sports and Entertainment, I am actually surprised that 6% of respondents showed any level of approval with KSE.

THE PHASES OF PLAY:

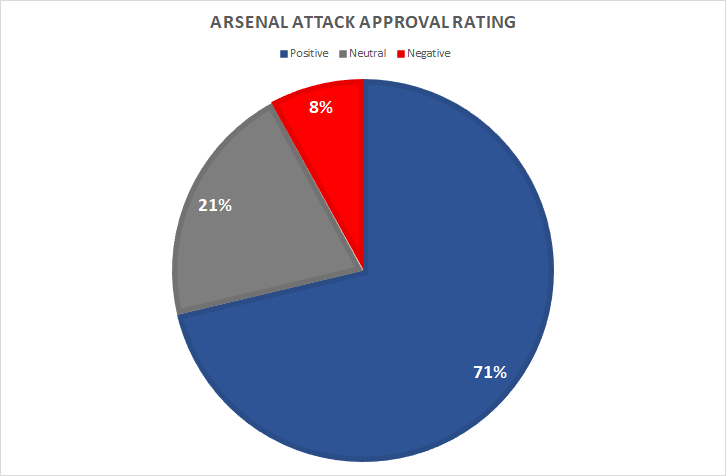

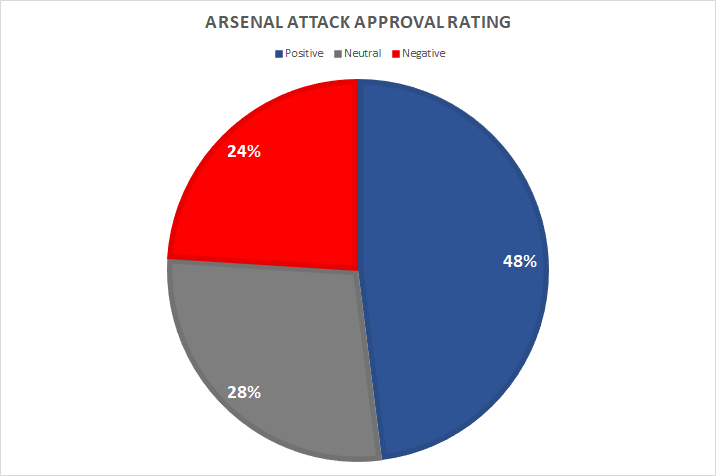

The approval rating for the attack improved quite a bit from the last time I asked. Arsenal did score 13 goals in the time between surveys averaging 1.9 goals per match, which was a significant improvement over the 1.3 that they had in the last survey period so maybe that explains things.

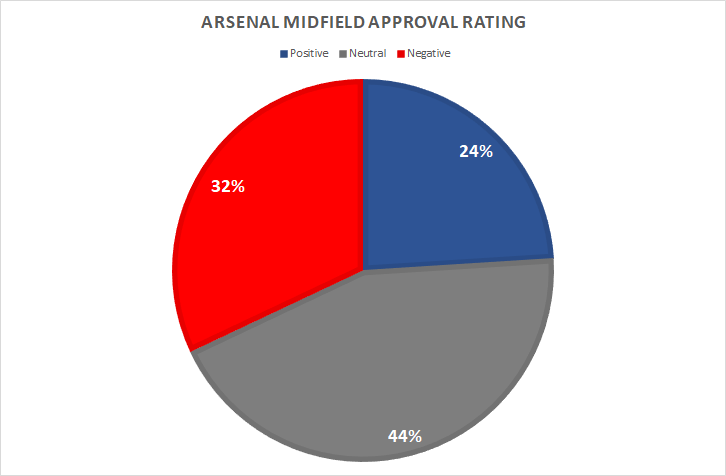

For the midfield, things are still generally mixed and there hasn't been much change since the start.

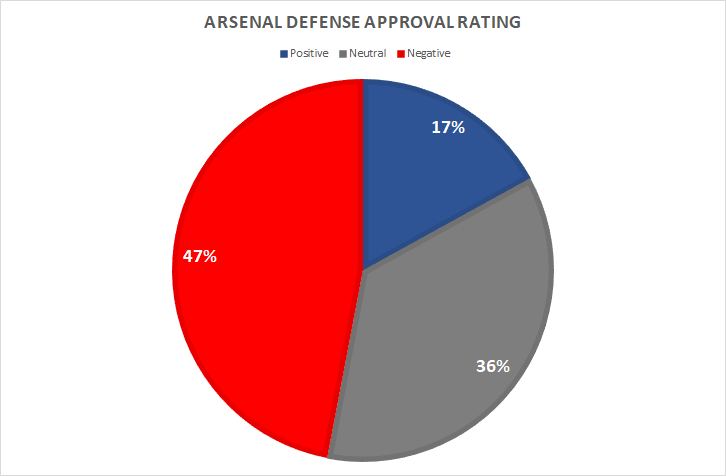

In defense, things have shown steady improvement. Fans are still generally negative about the Arsenal defense but the trend is very positive. That is also reflected in the statistics for goals allowed, Arsenal allowed just 0.7 goals per match in the 7 matches between surveys and in general I think that they have looked like that isn't a fluke.

Happiness Index Report: January 28, 2020

by Scott Willis

The second update to how you all as fans are feeling about Arsenal are ready to go. We got a few less responses but still have a sample of over 500 respondents, which while not a perfect sample is better than nothing and hopefully it will grow as time goes on.

With this being the second version we also have a baseline from two weeks ago to compare to, so that will be interesting to add as well. Without further bloviating lets get into the numbers.

General Arsenal Approval Rating:

The plurality of respondents still feel positive about Arsenal however there is a significant drop from 67% approval to just 41%. In the intervening time Arsenal collected 3 draws, haven't really done much in the transfer window (not even really any sexy transfer rumors) and perhaps some of the honeymoon period of a new coach is wearing off (but perhaps not looking at Arteta's approval rating).

Arteta Approval Rating:

Arteta is still very popular with the Arsenal fans. He too has seen some decline with his approve a great deal declining from 86% to 61% but overall he is still at 98% approval which is still about as good as is possible from a head coach.

The Management Duo:

Raul and Edu have both seen their numbers drop quite a bit since the last survey. Raul has gone from a plurality approving of the job he is doing to a majority disapproving of the work that he is doing. I can't exactly point to a reason why things turned so much in the last couple of weeks (maybe transfers?, general lack of a team building plan?, he's the face of the management team and getting the blame going towards the Kroenke's?) but Raul now has more people that "Dispprove a great deal" than he has in the combined "Approve a great deal" and "Approve a moderate amount". This will be an interesting one to watch as time goes on.

Edu still is overall neutral, but as people form an opinion people are breaking towards disapproving. He still seems to have a secondary role on things to Raul and maybe that is why he isn't getting quite as much blame.

The Phases of Play:

The approval of either the players or the style (I don't specify in the question) is another area where things have gone south quickly. The Attack went from wildly popular to just a plurality approving. The negative feelings have gone from just 3% to 24% in the space of two weeks. Maybe people had different expectations for what Arteta would be able to do with the Arsenal attack but whatever it is, people have turned pretty quickly on it.

In midfield it is more of the same. I am pretty confused about this one as well as things haven't really changed much and honestly I think that you can see much better structure in the way that the team sets up and while there hasn't been massive improvement in the attack, there has been noticeable improvements in midfield control turning into less shots allowed.

The defense, well everyone knows that is a problem and there isn't really much change since the last time.

That's it for this time. After the next set in a couple weeks we can start to see if some trends emerge!

Happiness Index Report: January 8, 2020

by Scott Willis

I asked people to fill out their opinions on how they felt things were going at Arsenal earlier this week, now it is time to take a look at the results.

First let's take a look at the general feeling that people have for the team:

I don't have the data for it (thus why I started this) but I bet a month ago things would be vastly different. Currently two thirds of Arsenal fans who participated in this survey feel positive about Arsenal, breaking that down a little further 6% felt very positive about Arsenal currently. 10% of Arsenal fans had a negative view of the team but less than 1% had a very negative view. In general, I would feel comfortable saying that the early results and performances under Mikel Arteta have made people feel a lot better about the direction of the team.

The head Coach:

I am sure there are still holdouts who aren't sold on Arteta for some reason or another but those people didn't get included in the nearly 600 people who ended up taking this survey. Overall only 0.5% of respondents don't approve of the job that Arteta is doing. This is for sure the honeymoon stage and unless things go perfect it is unlikely that he will be able to have near unanimous support among fans.

Head Of Football

Arsenal's Head of Football, Raul Sanllehi does not share the same level of support as the head coach. If we looked at this following the summer transfer window maybe things would have been more favorable for him but the narrative that came out during the last months of the Unai Emery reign was that he was still a believer in him (going so far as looking to extend his contract in the summer) and it wasn't until almost all hope of top 4 was gone that he seemed to be convinced that a change was needed. From my own perspective, this plus still being uncertain about his transfer style of agent contacts has me on the fence about him. The fall from "Don Raul" has been pretty swift.

Director of Football:

Edu is the second newest member of the Arsenal management team but he has the least publicly defined role (besides looking great in a suit for official club duties) and that shows in these ratings. This will be an interesting one to watch as time goes on.

Arsenal's Attack:

This isn't a surprising result to me, Arsenal's talent is heavily concentrated in the attacking side of the ball and the early results from Arteta is that he is going to do things to unleash them. I do have some sympathy for the 3% who have negative feelings about Arsenal's attack because even though things look like they are going to be moving in the right direction, this team still feels below where we have seen Arsenal in the recent past.

Arsenal's Midfield:

I was a little surprised by this one. I am in general fairly positive about Arsenal's midfield and I think that the early results of Arteta show that their is talent there if it isn't misallocated and played out of position. Maybe the plurality of people are talking a wait and see approach to this. I do think that this will be an area that Arsenal will need to strengthen in the summer but there are talented players here.

Arsenal's Defense:

That the defense has the lowest ratings is not surprising. This is the biggest weakness in the current team and has been for a number of years, probably going back to when Mertesacker and Koscielny were in their primes. 17% of respondents had a very negative view on Arsenal's defense, so to get some easy gains going from a disaster at the back to just bad would be helpful. Some strengthening in January, even it was just a loan, would probably also be welcome according to Arsenal fans.

That's it for this week. Thank you to everyone who took the time to fill out the survey. I will look to do another one of these in 2 weeks and then on a continuing basis to be able to track the trends. I might add some questions along recruitment and maybe a couple other things but i still want to keep this to a quick survey to encourage as many as people as possible to fill it out.

An American Gooner In North London

The Decision

When considering what me and my lovely girlfriend should do for holiday this year, our initial thought was to vacation to Spain and to spend a nice 10 days in Barcelona. After a brief search on the most popular travel sites, we realized quite quickly that $2,000.00 in return tickets alone was not as appetizing as the allure of the warm Catalonian sunshine. We happen to live in Long Island, which is right outside of New York City, so we ultimately had an easy flight path to Europe.

Our next thought was to visit the south of France, a beautiful vacation to the Côte d'Azur better known as the French Riviera. After another seemingly endless search trying to discover reasonable flights, we discovered this journey was also too expensive for only 10 days.

A look at the start and end dates of our holiday lead me to a very interesting discovery. We just so happen to be planning to head to Europe during the opening game of the season at the Emirates vs Burnley!

After what seemed to be endless searching which coincided with some careful budgeting on our side, I had a stroke of brilliance. What if I could somehow do a train tour around Europe that started in London? Could I sell that to my better half?

The answer was yes… what follows is my experience.

I will attempt to depict my pilgrimage to the Emirates. I will attempt to encapsulate my thoughts and feelings in a coherent manner. I will attempt to make some suggestions for folks who might also be making their first trip in the near future.

The challenge with all of that is, if you love the club the same way that I do, this task is seemingly impossible. For a foreign fan, watching the team week in and week out, living and dying by the pixels on a tv screen or laptop monitor – seeing the Emirates for the first time is a surreal experience. Come on the journey with me ya gunners.

The first question is..

How do I get tickets?

Once I convinced my girlfriend to gallivant to London with me to visit the Emirates, I had a big task at hand, how do I purchase tickets.

This is not such a straightforward experience to the layman. After some careful investigation, I learned that purchasing tickets from popular ticketing websites may be illegal in the UK. This was a complete shock to me as third-party ticket reselling in the US is the most common mechanism for purchasing match day tickets – for any sport. This had me a bit rattled, so I decided that the best approach was to go directly to https://www.arsenal.com/ to purchase tickets.

What I did not know was that in order to purchase tickets from The Arsenal you must go on their Ticket Exchange which is a marketplace for reselling directly through the club. In order to gain access to the ticket exchange, you must purchase a membership plan which will grant you access to the ticket exchange – the better the membership plan, the earlier in advance you can purchase tickets. Much to my chagrin, since this was fairly last minute (3 weeks before the match), I decided to purchase the red membership. This was essentially a £29 cost for purely the chance of purchasing a ticket. (You can find out more about red membership details here https://www.arsenal.com/membership/red)

Bad luck for me though…

All of the tickets were sold out on the ticket exchange and my dream was almost shattered. I decided that this was not enough to get me down and that after all of this hard work and planning, we would take the risk and purchase tickets via StubHub. After two weeks of waiting, I received the email with our e-tickets!

The next question we had to ask ourselves was…

Where do we stay?

Luckily for me, working for global companies for the better part of my career left me with friends that lived in and around London. The recommendation that was given by a good friend and colleague was to stay in Shoreditch. Shoreditch is a hipster part of London that is located in the borough of Hackney. We stayed around a very reasonably priced area in Shoreditch which was roughly a 12-minute uber ride to the Emirates stadium. Our hotel was very accommodating with nice restaurants, clubs and bars nearby… not to mention some great street art:

The Emirates Experience

Once gameday arrived I donned my bruised banana Arsenal away kit and made my way towards the stadium. The game was set to start at noon, which left me at a decision point of what time to arrive. We arrived two and a half hours early so that we had plenty of time to take in the surrounding ambience that was North London. Traveling to the stadium in our minicab, we traversed Holloway Road that brought us past Highbury and into Islington (names of the local towns in the area – probably familiar to most). As we made our way through the streets, we were brought into a neighborhood where our Uber driver instructed us to exit. After walking up a block or two we were able to see it… finally.

The first thing you see as you walk up to the stadium is the Armoury.

The Arsenal Armoury

Once you enter the Arsenal team shop, you walk into a room that has all the kits anyone could ever dream of. In the main entrance area, there is all of the Men’s kits, these varied from warm ups to the standard Home, Away and Alternate jerseys.

Even roughly two hours before kickoff the Armoury was packed! There was a substantial amount of families. While wandering around and casually shopping I was able to meet Gooners from all around the globe. We met many Gooners that varied from countries such as Australia, Japan, Nigeria – we even met fellow Americans from Colorado and Boston. I must warn any first time Gooners that there is a metric ton of awesome Arsenal memorabilia and clothing – please be prepared to spend money if you walk in there. I personally got a custom printed Bergkamp #10 on the home kit, which was around a 20-25-minute wait (view from the line below).

This whole experience gets you really jazzed for the game. As I walked out of the Armoury I felt this feeling of anticipation welling up inside of me, I was a few short steps away from entering the stadium grounds where the new look Gunners would face Burnley.

As we walked up the stairs, we were greeted by music…

Entering the grounds

Once we climbed the staircase that led to the main promenade, we were greeted by a quartet of brass players playing on a stage. They were playing a lively tune that flittered through the warm summer day, saluting the fanbase on their way through security. While we walked and wandered towards our preferred entrance, a nice woman came up to us and handed us a card for a free pint of beer inside the stadium. This turned out to be Arsenal’s new brewery sponsorship, Camden Town Brewery.

Before walking into the grounds, I stopped for a moment to take the whole beauty of the stadium in, there is a giant mural of some legends that look over the stadium from the upper perches of the walls (History Through Harmony):

After the initial butterflies of being there had subsided to a degree, we walked to our “gate” and walked through security. The experience of passing through security for me was very light compared to what I am used to in the US sports venues. A quick look through our bags was all it took for us to be passed through to the turnstiles. We were quickly into the inner sanctum of the Emirates.

Inside the Emirates, we saw a ton of concession stands and food halls. It is important to note that we had entered on field level and this account is from that purview. Needless to say, at this point, the anticipation of getting my free beer and walking onto the field level seating was growing. We quickly grabbed our free Camden Town Brewery lagers and headed for our seats.

One thing to note that was also a bit of a shock to me, was that, alcohol was not allowed on the field facing portion of the stadium. This may seem naïve to folks who grew up in Europe and attended many football matches abroad, but this is a completely different policy compared to American sports. This is an important memory to point out because it required me to drink my beers quickly inside the stadium prior to heading to my seats. This probably added to the liquid courageous feeling that I felt when I actually saw the field.

My view from our seats – NorthBank

The Atmosphere

Walking out and seeing the Emirates field for the first time is very difficult to explain. Arsenal Football Club has become a sort of obsession for me over the course of the past 5 years or so – watching and admiring the ups but mostly the downs over the course of the past decade. This summer on the other hand left the club in a positive light for the first time in a while. The business that was done left a sense of optimism in the air and it resonated throughout the pitch.

It may sound odd to the say that being there in person was euphoric but that is really the best way to explain it. Once the match began, being so close to Aubameyang, Ceballos, Guendouzi, Leno, Sokratis, etc… at times I had to pinch myself to make sure I wasn’t dreaming.

The result of the match and the overall tone of the game also assisted in enjoying the experience thoroughly. This includes but is not limited to the stadium energy and the banter all around me. We had heard in the past that the Emirates is quiet and lacking in charisma but that was not the case on this day. The four-tiered bowl that comprised of roughly 55,000 screaming fans was both beautiful and electric. Our perspective was from the North Bank, closer to the field level by the corner flag. I mean just look at some of the photos:

Aubameyang and Mike Dean – bitter rivals)

Post Aubameyang second half goal

An American Gooner in North London

Being a tourist in London for the first time let alone traveling to the Emirates can be intimidating. Especially since it is difficult to answer some of the questions mentioned earlier in this blog post. Hopefully some of this helped someone, somewhere looking to visit for the first time and to emulate this experience. Hell this might even be interesting for locals and season ticket holders – to understand what visiting the stadium means to someone living 1,000’s of miles away.

Being somewhere you’d never thought you’d get to be is special. Being there with the person you love is life changing. Getting to share that experience with countless others in this beautiful community we call fandom – priceless.

North London is red my friends, I just had to see it with my own eyes.

Arsenal vs. FFP in 2019/20 - Are We Screwed?

by Tom Jones

FFP SUMMARY

To comply with Financial Fair Play clubs must break even or better on a rolling three-year aggregate. For example, to qualify under FFP in the 2019/20 season the club submits total profit and loss (P&L) from 2016/17, 2017/18 and an estimate of 2018/19 (official accounts are not available when submission is due). For 2020/21, the accounts for 2016/17 will be replaced with estimates for 2019/20 and so on. Owners can offset losses as much as 35m per year with cash investment, and clubs can deduct expenses on youth development and infrastructure from the calculation.

Seems reasonable, right? But as we will see, there can be some unintended consequences of this three-year window that clubs may not have anticipated. In Arsenal’s case, a large cash reserve was built up long before FFP as Arsene Wenger and the board kept player trading expenses down. Arsene finally started to spend the cash, but as of May 2018, Arsenal still had about 195m in “free cash.” We have repeatedly heard from management that money generated by the club is free for investment into the squad, so why in January of 2019 when faced with a tight race for the lucrative Champions League and key injuries did the club state it could only loan players while sitting on 200m?

One prevailing theory is that Stan has tightened the purse strings to cover cost overruns at his LA stadium project. While a nice narrative, there is another possible explanation—that the fiscally responsible Arsenal are up against an FFP wall. As I’ll explain, the player trading and contract management at Arsenal the last few seasons have put the club in an accounting bubble which has ballooned and effectively made spending the cash pile very challenging even if KSE has given the green light to use it. To see this, we will need to first understand how the club accounts for player trading.

PLAYER TRADING ACCOUNTING

As fans we like the simplistic approach of following the cash balance numbers and annual “net spend” figures that are spouted in the articles we read. In truth though, there is no such item in the official accounts. Player purchases, renegotiations and sales are distinct types of transactions and are accounted for differently in both amount and timing.

Player Purchases

While a club may pay actual cash for a player’s registration from another club, this cash paid does not immediately go toward expenses (see highlighted portion of Official Arsenal Accounts below). This is because the new player’s registration is considered an (intangible) asset, and for accounting purposes the cost of assets is realized over their “useful life.” While the “usefulness” of some of Arsenal’s players is debatable (ahem, Mustafi), the club will spread out or amortize the cost of a player’s registration over the duration of the player’s contract.

This is useful for typical businesses so that when acquiring a large asset, they can spread that cost out and not take a huge hit on the bottom line in a single financial period. But typical businesses don’t have to deal with FFP, and Arsenal do.

As an example of how this is done, we can look at the purchase of Alexis Sanchez by Arsenal. He was bought for reported 35m in 2014 on a 5-year deal. That 35m did not go on Arsenal’s P&L for 2014 as an 35m expense, however. Instead, Arsenal booked his registration as an intangible asset with a cost of 35m. Each year for the term of the contract they amortized that value down by 7m (35m/5yr) and booked the 7m as an amortization expense (see the line item below). So, in terms of affecting the P&L, and therefore FFP calculations for that season, Sanchez only “cost” the club 7m in 2014 even though they might have paid the 35m up front in cash. Of course, this meant he was still hitting this line item for 7m in 2016 as well.

Contract Renegotiations (extensions)

In these situations, club accounting policy (see below) is to take the remaining amortization of the player’s registration (what’s left to expense from the initial purchase or prior renegotiations), add that to the cost of the new contract (certain bonuses, Agent’s fees, etc.) and then amortize that “total cost” over the life of the new contract.

Consider the Ozil deal. At the time, Ozil had about 6 months left on his original cost of 42.5m. So, the club maybe had about 4m remaining to amortize. Certain bonuses to the player, agent’s fees for the new deal, etc. are added to that remainder (maybe 10m for such a huge deal). Therefore, we have maybe 15m as the total cost of Ozil’s current registration. The club will spread that over next 3 years (duration of his new deal) by taking an amortization expense of 5m every year. So Ozil hits the bottom line to the tune of negative 5m or more per year on top of his 18m per year salary. Easy to see why the club possibly wanted him off the books in January.

Player Sales

When a player is sold, the remaining amortization is subtracted from the sale price and the result is what hits the bottom line as either profit or loss.

Consider the rumored sale of Xhaka this summer for 50m. While the club might receive a check for 50m, that money will not contribute to the P&L as a 50m income. At the time of sale, the club must charge off the remaining amortization left on the player’s registration. As we learned from the sections above on purchases and renegotiations, the club is yet to fully realize Xhaka’s initial purchase price and he also renegotiated his deal in 2018 further adding to his “cost”. When he is sold, this remaining amortization would need to be realized which would offset some of the 50m income from his sale.

In detail, Xhaka’s original deal was reported as 35m for 5 years so the club was charging 7m off each year. At the time of renegotiation in 2018, the club still had 21m (7m per remaining year) left to amortize. He renegotiated for reported 5 more years. So, add another few million in agent’s fees and bonuses and you probably have 25m left. Subtract the amortization taken in 18/19 (1/5th) and you are left with about 20m or so to amortize at the time of sale. Therefore, if Xhaka is sold for 50m this summer, the club may see an increase in cash by 50m but will actually only book an income on the P&L of 30m from the transaction.

Again, for a typical business this is good. It can essentially shield the bottom line from huge fluctuations when a large asset is sold (i.e. dodge the tax man). However, these costs are being spread out over 5 or more years while profits from sales are being realized in one season. With only a three-year window for FFP it’s easy to see that occasionally this may cause a problem if not considered by management.

A prime example of how this disparity can unexpectedly affect the P&L can be seen in Arsenal’s spending in 17/18. At first glance the net spend in cash terms was close to zero (3m net income according to tranfermarkt.com) with sales of Giroud, Ox, Walcot, etc. essentially balancing out purchases of Auba, Laca, etc. However, due to these accounting practices, Arsenal actually booked a 120m income on player “disposals” that year (see P&L from 2018 below) which was only offset by player trading expenses of 91.7m. Essentially Arsenal only generate 3m in cash from player trading that year but booked a net positive of about 30m toward the bottom line.

How is this possible? Due to the accounting differences between purchases and sales we explained above, most of the cash from the outgoing players was booked as profit for 2017/18 while most of the cost of incoming players is spread out to future years. This is the problem Arsenal are facing with respect to FFP.

Another good example is the Sanchez/Miki swap deal with United. To the fan, it seems like a net-zero even swap since no cash was exchanged between the two clubs. However, for accounting purposes this was a sale of an asset (Sanchez) and a purchase of another asset (Miki). For this one, the club uses the fair market value of the players (reported as 35m in this case). So the club booked an income of 35m from the Sanchez “sale” for that year (less any remaining amortization). But for Miki, the club will spread the 35m “cost” over the 3.5 years of his contract (10m per year). The effect of this is that the club booked a “profit” on the exchange of perhaps 20m or more for the year 2017/18 even though no cash was exchanged.

Of course, there is no such thing as a free lunch, and the club still amortizing Miki’s registration at the clip of 10m per year and over time this will net out to zero. But, by taking the profit in one year and the expense in future years can really hurt the bottom line when the year of the profit drops out of the FFP calculation, but the years of the expense remain—essentially a 50m swing in this example. More on this in the FFP section below.

What is the consequence of all of this? From a business point of view Arsenal is actually doing okay in terms of revenue, cash and debt trends. But the way Arsenal have “timed” and structured their player trading in the twilight of Wenger’s reign means those deferred costs have created a bubble which is hitting the club’s P&L hard starting in 18/19 and likely continuing through 21/22.

FFP ANALYSIS

Now that we know how the accounts are handled, what does the FFP situation for Arsenal look like? Recall that according to FFP, Arsenal must profit or break even over a rolling three-year aggregate or face penalties. Let’s look at the next two seasons--2019/20 with the FFP window using accounts from 2016-19 and 2020/21 with the FFP window using 2017-20.